Introduction

Every investor has an investment thesis. At its core, it’s their “why.” Some say they invested because they believed in the team, others because they loved the technology. It could be because of the particular market, competitive positioning, speed-to-market, unit economics, or any number of combinations. All these rationales are valid — and in some cases common — ways to invest in an early-stage company, and collectively fall under the umbrella of what competitive edge a company has over others. While such rationales may serve as “an” investment thesis, they do not comprise a complete first principles-based investment thesis that drives venture-style outcomes.

So, what is first principles-based investing? This is a method of formulating a thesis where an investor:

- Understands the competitive landscape in depth

- Has sufficient knowledge of both present and future knowns/unknowns and is able to map the future arc of that landscape as a function of potential solutions

- Can identify what solutions will disrupt an entire industry, aka the disruptions likely to generate venture-like outcomes i.e. 100X in valuation jump from initial investment)

This future arc prediction allows investors to invest with courage and conviction — understanding all risks. In my case, it also allows me to avoid getting sucked into any fear of missing out (FOMO) or hype-based investing pitfalls.

first principles-based investment thesis (FIT)? It is aptly a bit like going to the gym and getting “fit.” It takes a lot of work, the results are not immediately seen, and yet it is tremendously good for long-term financial health.

Here is how we develop our FIT method.

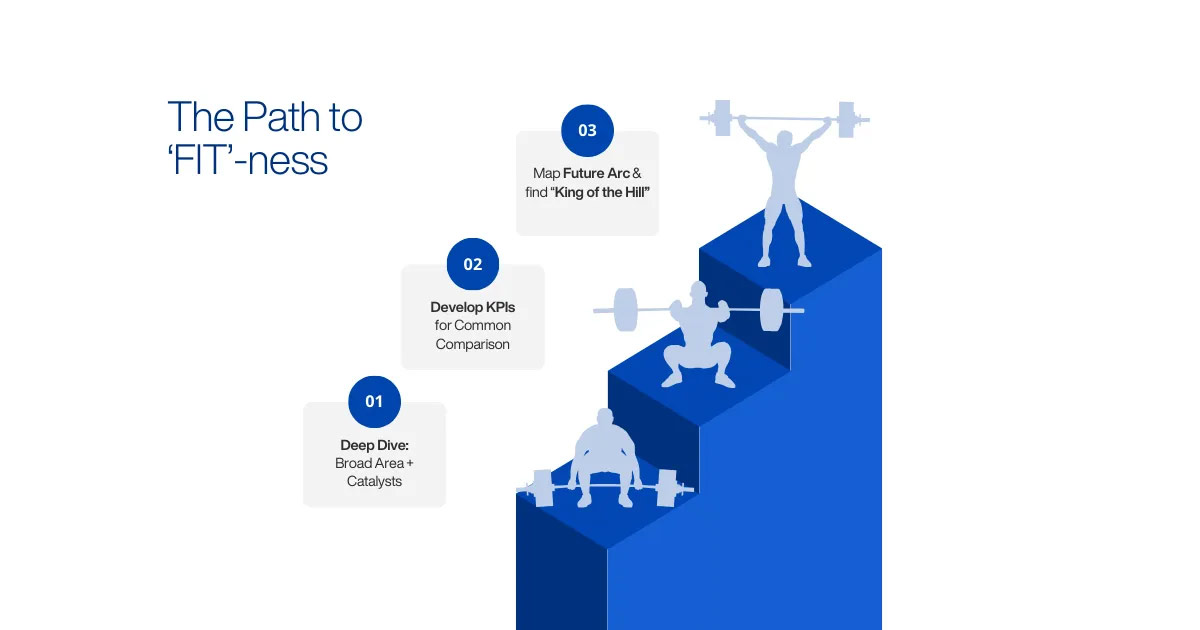

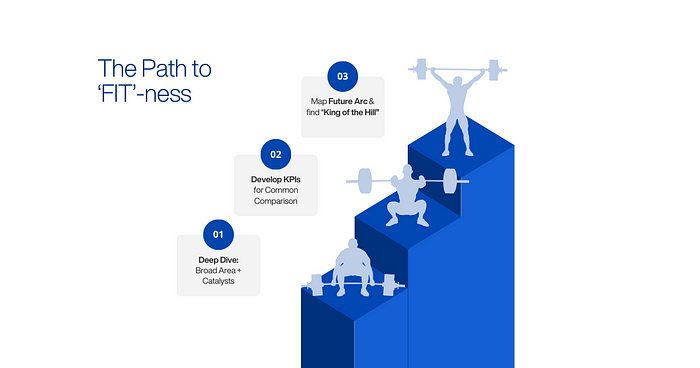

Step 1: DEEP DIVE — Scan the area to understand what is driving venture-like growth and incentives for incumbents to understand “why now” and “find the catalysts”:

The first area to map in the FIT method is to scan a broad area and understand the question “why now?” A broad area could be as vague as lithium extraction, space mining or textile recycling”. Once identified, ask “why now?”, then “why is this space going to take off exponentially now?” A technology platform can inspire an entire industry to mass adoption (like Apple Store unlocking an array of apps), or it could be in new regulation providing traction to an industry (like EV tax-credit motivating the electrification of consumer transport). It could also be a scientific breakthrough like CRISPR technology helping revolutionize genetic medicine development. We call these rationales “catalysts.”

Once you find the catalysts, it’s critical to understand the incentives and disincentives in the industry (or in specific geographies). Whenever incentives are aligned, incumbents with a large balance sheet may have a better chance to succeed over innovators. When the incentives are completely or partially misaligned, a new technology or business model stands a chance against incumbents. In my view, this is where information asymmetry can produce non-obvious insights — and an investment opportunity.

Many times, there is only a small window of opportunity for startups before the incumbents catch up. Sometimes, investor dry powder deployed can be a good surrogate to understand whether timing is right. Too many startups funded in a space? This is a good indication that incumbents are already mobilizing their resources. Smart investors deeply understand this window and time their investment based on their FIT. If we cannot answer “why now” and find a credible catalyst, we usually stop right there as this usually means: a) we do not have enough insights to make an investment; or: b) we do not believe this will produce venture-style financial returns.

Step 2: DEVELOP KPIs — Gain a strong understanding of the competitive landscape and organize the market based on the constituent KPIs to develop a preliminary investment thesis

Once we develop a strong understanding of “why now” and “why a startup has a chance to succeed,” we spend a good amount of time speaking with as many startups as we can. In this research, we are looking to understand the right benchmarks on technology, product, scale-up, commercial, and company-level KPIs. It’s like the composition of a complex piece of music, with different instruments with various intonations and knobs that need to be turned up and down based on time to market. If we think of each of these metrics i.e., technology, product, scale-up, commercial, and company-level KPIs as a dial knob of 0–10, an early-stage company may have a great tech and product but may score low on scale-up and commercial fronts. This is in contrast to a later stage company, which might have better scale-up and commercial numbers but may or may not have a great technology. At this point, we can start developing a preliminary version of a FIT. This part — developing KPIs from different technical approaches — can be an arduous task, especially when there are multiple ways of solving the same problem. The best investors in my view know exactly how to compare apples with oranges and tell you which one is better for that situation.

Step 3: MAP FUTURE ARC and FIND “KING OF THE HILL” — Find the “King of the Hill” by validating and invalidating the hypotheses built using FIT and invest by understanding the full dynamic range of possibilities (what can go wrong and what happens when everything goes right)

After conducting thorough research, our goal is to accumulate all potential solutions to the problem and rank-stack each solution with their component KPIs (tech, product, scale-up, and commercial). The next stop is for us to find the “King of the Hill”– or the company most likely to be the market leader in 5 to 7 years. For that, we must first define what the “Hill” really is. Depending on the situation, it could be geographically based (like US, EU etc.), application-based (like EVs or data centers etc.) or other definitions (the bigger the hill, the larger the investment outcome / risk usually). Once our “Hill” is defined, we envision an “arc of the future” pending disruption of various technological advances, product updates, scale-up, and commercial maturity from various companies. Drawing an arc like this many times requires us to go deep into a handful of companies and doing more comprehensive due diligence (DD). During our Deep Dive process, we try to evaluate any preliminary FIT hypotheses we have developed, validating or invalidating each which strengthens our final FIT position.

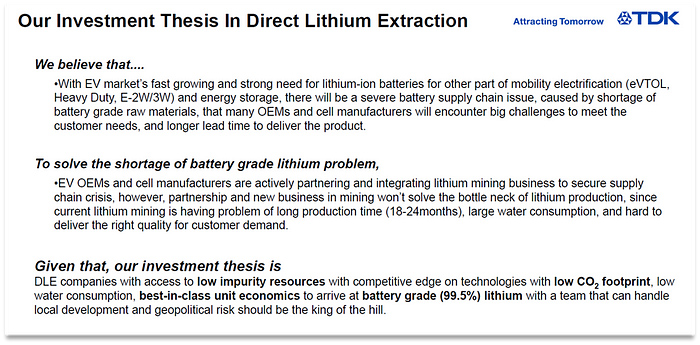

We then state our knowns, unknowns, beliefs, and hypotheses to lay out our first-principles-based investment thesis clearly like the one we have shared below for our direct lithium extraction (DLE) company Novalith.

In Novalith’s case, we saw many companies in the DLE space producing non-battery grade lithium products with unit economics susceptible to lithium price changes in geopolitically challenging environments — with feedstock having low lithium concentration. After our research, we built conviction around Novalith as the company was generating battery-grade lithium in Australia with high concentration spodumene ores, and with these supporting attributes became our “King of the Hill”.

While establishing a fit overwhelmingly helps us make our selections, it doesn’t guarantee a great investment that will help return the fund every time. All those other factors — such as the “whys” above — matter. Amazing teams, technology, product, scale-up, and track record all lends to what makes a phenomenal company. But they also lend to what makes for a too-obvious investment case. Likely such an investment doesn’t exist in the early stages of a company. If it does, then the pricing is potentially too high for the ownership targets that most early investors have. The trick is to identify the right exceptions to make and understand the full dynamic range of possibilities of what could happen. This includes if everything goes wrong and what happens when everything goes right.

The FIT method is by no means a perfect. There is still an “art” to investing — and we aren’t always correct. But, without having the FIT method, we would be investing in the dark and not sufficiently prepared.

The best entrepreneurs deserve to work with investors who come prepared — not just for financial milestones but along the way.

Preparedness and delivering deep insights is a TDK Ventures core value, and we are extremely proud of using our critical thinking acumen in making such tough investment decisions that change the world.

After all, as Steve Jobs said, “The people who are crazy enough to think they can change the world are the ones who do.”