By Katherine(Qianran) He and Adam Erlichman

We’ve closely tracked the evolution of U.S. federal legislation in 2025 and its wide-reaching implications across the cleantech landscape — from critical minerals to grid storage and hydrogen at TDK Ventures. The passage of the “One Big Beautiful Bill” (OBBB) has provided long-awaited clarity on several fronts. While the legislation includes cuts that will be felt across the energy transition, it also preserves — and in some cases expands — support for key segments of the ecosystem.

This document outlines the key clean energy-related provisions of the OBBB and their likely impact across technologies, markets, and timelines. In particular, we highlight how grid-scale storage, geothermal, and critical minerals emerge strengthened; while solar, wind, and EVs face accelerated credit sunsets and tighter compliance rules. We also provide insights into how domestic content requirements and FEOC (Foreign Entity of Concern) restrictions will shape supply chains going forward.

At TDK Ventures, we remain committed to actively investing in great cleantech founders; we also continue to support our current founders with unwavering enthusiasm. If you’re choosing to continue fighting the good fight, let’s chat.

—

“An Act” — referred to as ‘OBBB’ throughout this piece — is a $3.4 trillion budget reconciliation House Bill signed into law on July 4, 2025. It contains tax cuts, a $5t debt ceiling increase, clean energy policy restructuring, and a $100b expansion for DoD funding. It also includes healthcare provisions, infrastructure spending, immigration enforcement funding, education policy modifications, extensive deregulation, and other items outside the scope of this writing. The full piece of legislation can be found here.

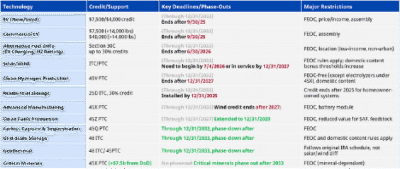

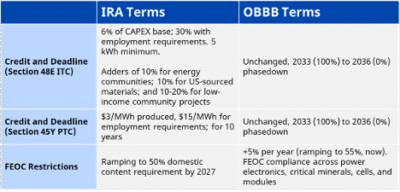

The following table provides a high-level executive summary of the key energy-related provisions in the OBBB, organized by technology segment. It highlights the available credits or support, phase-out timelines, and major restrictions — especially those related to domestic content and Foreign Entity of Concern (FEOC) rules.

Summary Table

*Most of the FEOC (Foreign Entity of Concern) restrictions under the OBBB Act begin applying from the beginning of new tax years post 7/4/2025. Some credits (like grid-scale storage and geothermal), have bonus adders (domestic content, energy community) that can increase the ITC up to 50% if eligibility criteria are met.

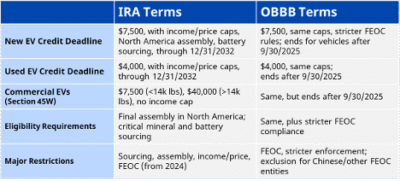

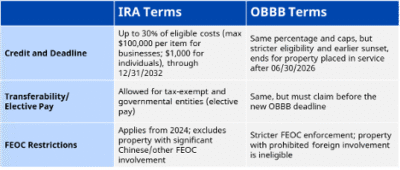

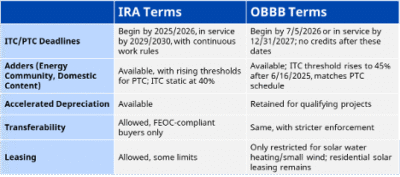

To support deeper analysis, the subsequent tables compare OBBB terms with those of the Inflation Reduction Act (IRA), providing a side-by-side view of policy shifts, eligibility changes, and potential impact by sector.

—

↓ EV Incentives

- Deadline: All EV credits — consumer and commercial — expire for vehicles acquired after September 30, 2025. (This does not include charging infrastructure.)

- To qualify before the deadline, vehicles must meet final assembly, critical mineral sourcing, and FEOC (Foreign Entity of Concern) requirements.

- The accelerated sunset of both consumer and commercial EV credits sharply reduces federal support for new electric vehicle purchases after September 2025.

- Cities and companies must act quickly to secure credits for fleet electrification before the window closes.

—

↓ Alternative Fuel Infrastructure

- Businesses and individuals must verify that their installation site is in a qualifying tract to claim the Section 30C credit for EV charging or H₂ fueling infrastructure.

- Non-qualifying locations are ineligible for the federal credit, regardless of other project merits.

- Prevailing wage and apprenticeship requirements must also be met for the full 30% business credit.

—

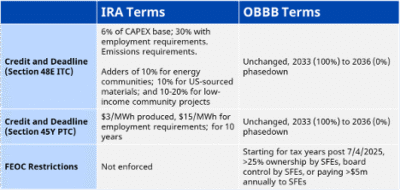

↓ Solar and Wind Incentives

- Projects that do not meet the new OBBB deadlines are ineligible for credits, even if they would have qualified under prior law.

- All solar and wind projects claiming credits are subject to Foreign Entity of Concern (FEOC) rules, barring credits for projects with significant Chinese, Russian, Iranian, or North Korean ownership, control, or supply chain involvement.

- OBBB addresses a prior legislative glitch: for ITC projects, the domestic content threshold increases to 45% for projects beginning construction after June 16, 2025, with annual increases to match the PTC schedule (up to 55%). Projects that began construction before June 16, 2025, can still rely on a 40% threshold.

—

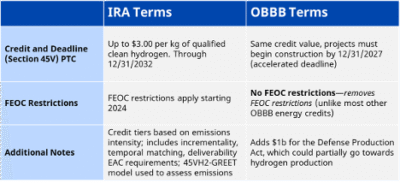

↔ Hydrogen Production

- OBBB allows hydrogen projects to use FEOC-linked electrolyzers and still claim 45V, but the electrolyzer itself will not qualify for 45X manufacturing credit if it’s from a FEOC during tax year beginning after 7/4/2025.

- Projects must still meet strict lifecycle GHG emissions thresholds (0.45 kg CO2eq per kg H2 for highest credit), prevailing wage, and third-party verification requirements to claim the full credit.

- The technical calculation, verification, and documentation standards remain largely unchanged from the IRA, including the use of the 45VH2-GREET model and EACs for electricity sourcing.

—

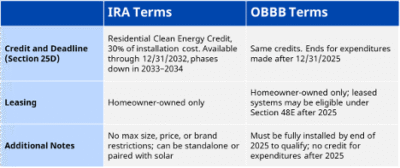

↓ Residential Energy Storage

- If the residential energy storage system is leased from a third party (not homeowner-owned), it may be eligible for the Section 48E Investment Tax Credit after 2025. In this case, to qualify for the domestic content bonus (an additional 10% ITC), the project must meet rising domestic content thresholds:

- 45% U.S. content for projects beginning construction after June 16, 2025

- Threshold increases annually, reaching 55% for projects beginning after 2027

- Both IRA and OBBB require a minimum battery capacity of 3 kWh and exclude systems with significant foreign entity of concern (FEOC) involvement.

—

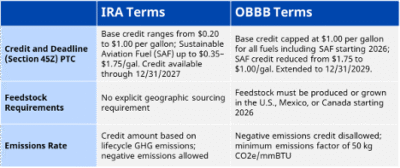

↔ Clean Fuels Production

- The OBBB extends the 45Z credit by two years but reduces the maximum value for SAF and imposes stricter feedstock sourcing and emissions rules.

- Starting 2026, only fuels made from U.S., Mexican, or Canadian feedstocks are eligible.

- Negative emissions rates no longer increase the credit above the maximum cap.

- FEOC (Foreign Entity of Concern) rules continue to apply, but only for ownership, not material assistance.

- Double-dipping with excise tax credits is prohibited under OBBB.

- Transferability is retained, and the IRS/Treasury will issue further guidance on implementation.

—

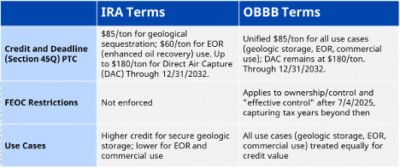

↑ Carbon Capture & Sequestration

- Construction window and 12-year credit period are unchanged from the IRA.

- Transferability: Both IRA and OBBB allow credits to be sold to third parties.

- FEOC Rules: OBBB applies only ownership-related FEOC restrictions (not material assistance), making compliance somewhat simpler than for other credits.

—

↑ Grid-Scale Storage

- Grid-scale storage (we will refer to this as ESS here) is intentionally spared from the cuts wind and solar face: “© EXCEPTION. — This paragraph shall not apply with respect to any energy storage technology which is placed in service at any applicable facility.”

- FEOC restrictions on the various components and raw materials behind ESS will require supply chains to be re-routed through non-FEOC countries. OBBB adds a 75% material assistance threshold by 2030, which is higher than other types of qualified facilities

- Domestic content restrictions will push for further onshoring across ESS supply chains

—

↑ Geothermal

- Construction window and 12-year credit period are unchanged from the IRA. Geothermal emerged as a clear winner from the OBBB, driven by Chris Wright’s pushto add its credits back.

- FEOC restrictions will complicate an already-complex project development process. This will create a need for supply chain audits, entity structure reviews, and material assistance monitoring.

—

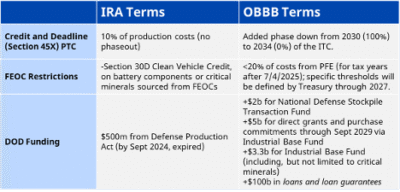

↑ Critical Minerals

- Companies must complete FEOC compliance audits by 2026 to qualify for 45X, which isn’t feasible in areas whose supply chains are dominated by China (like graphite); though it’s possible the Treasury will set more realistic FEOC thresholds for these minerals.

- The 45X funding is secure, but will begin phasing down from 2030.

- There is a massive new opportunity in critical minerals through direct grants/purchases ($3.3b), National Defense Stockpile ($2b) and $100b in loan guarantees. These make critical minerals a rare winner from the OBBB.

—

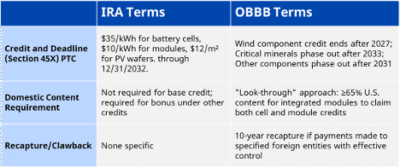

↓ Advanced Manufacturing — 45X

- Most U.S. battery producers will need to rapidly reduce FEOC (especially Chinese) content in their supply chains to remain eligible for the 45X credit, as the allowed percentage shrinks each year. The law uses a percentage-based “material assistance cost ratio” (see next slide) to determine eligibility for the tax credit. If the FEOC share exceeds the annual threshold, the product is ineligible for the credit for that year.

- Supplier certifications and detailed cost documentation are required to demonstrate compliance.

- Expanded definitions under OBBB allow more battery module hardware to qualify. Battery module definition expanded to include essential equipment (e.g., voltage harnesses, collectors), but all projects must maintain rigorous compliance and documentation to avoid recapture penalties.

—

Closing

Cuts to new energy technologies may seem dangerous for climate change and counterproductive to the administration’s Energy Dominance north star. It also raises the question of whether we’ve learned from past failures to build domestic solar and ESS production capacity. (Solar and ESS accounted for 84% of new US electricity generation capacity in 2024. Sadly, less than 10% of those ESS cells were made here in 2024. Additionally, as of 2022, a striking 88% of our solar panels were imported.)

Nonetheless, we continue. In our financial diligence, we assume zero subsidies across all scenarios. If our models are right, our portfolio companies will continue to be successful and carry the energy transition forward. The OBBB doesn’t mean Peak Energy or Ascend Elements are done writing the story of the future of US batteries. It doesn’t mean Verdagy or Ineratec will stop on their pursuit of decarbonizing hydrogen and fuel production. And it certainly doesn’t mean that passionate builders considering launching cleantech companies should hold back.

We continue to believe there is an asymmetrical opportunity in supporting the future of clean, abundant US energy.

Credit: RMI